Inflation clouds Bangladesh’s 5% growth outlook

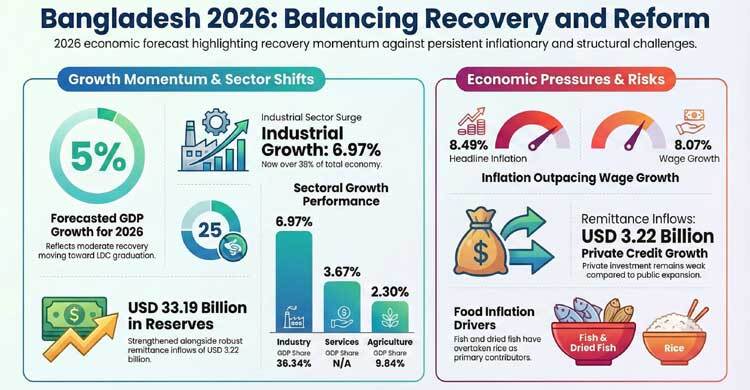

Bangladesh’s economy is forecast to grow by around 5 per cent in 2026, reflecting moderate recovery momentum amid persistent inflationary pressures and long-standing structural challenges, according to the Economic Update & Outlook for January published by the Planning Ministry.

The report, prepared by the General Economics Division (GED) of the Bangladesh Planning Commission, says sustaining growth will depend on stronger governance, policy consistency and increased investment in skills and technology to reduce the economy’s heavy reliance on the readymade garment (RMG) sector.

These reforms are becoming increasingly important as Bangladesh moves closer to graduating from least developed country (LDC) status and navigates a period of democratic transition.

Growth outlook and risks

The GED stresses that political stability, institutional reform and effective use of technology are essential to shift the economy away from a low-cost labour model towards higher value-added activities. However, uncertainty among economic elites and institutional weaknesses remain major risks to long-term growth.

Progress towards achieving the Sustainable Development Goals (SDGs) also remains slow. The report suggests that evidence-based policymaking, supported by targeted village-level interventions, could help deliver more sustainable development outcomes at the local level.

Inflation remains elevated

Inflationary pressures continued in December 2025, with headline inflation rising to 8.49 per cent, up from 8.29 per cent in November, driven largely by higher food prices amid persistently elevated non-food inflation.

Food inflation rose from 7.36 per cent to 7.71 per cent, while non-food inflation remained high at 9.13 per cent. Although rice inflation eased across all categories, prices remained elevated and continued to exert significant pressure on overall food inflation.

Overall rice inflation declined from 12.26 per cent in November to 11.92 per cent in December. Medium rice inflation fell to 10.48 per cent, fine rice to 14.84 per cent and coarse rice to 10.92 per cent.

Rice’s contribution to food inflation declined from 40.28 per cent to 37.34 per cent, while fish and dried fish became the largest contributors, rising sharply from 40.77 per cent to 43.34 per cent. Vegetables continued to have a strong disinflationary effect, with their negative contribution deepening further. Potatoes remained a major disinflationary factor, while onions shifted from a negative to a positive contribution.

Wage growth lags behind prices

Price inflation continued to outpace wage growth in December, widening the gap between household incomes and living costs. While price inflation increased by 0.20 percentage points, wage inflation edged up only marginally from 8.04 per cent to 8.07 per cent, signalling growing pressure on real purchasing power.

Recent growth performance

According to provisional quarterly national accounts data from the Bangladesh Bureau of Statistics (BBS), real GDP growth in the first quarter of FY2025–26 rose to 4.50 per cent, compared with 2.58 per cent in the same quarter a year earlier.

Overall GDP growth at constant prices reached 3.72 per cent in FY2024-25, based on provisional estimates.

Sectoral performance showed broad-based improvement. Agricultural growth turned positive at 2.3 per cent after contracting in the same quarter of the previous year. Industrial growth accelerated sharply from 3.59 per cent to 6.97 per cent, while growth in the services sector improved to 3.67 per cent, supported by transport, accommodation and information services.

The structure of the economy continued to evolve, with agriculture’s share of GDP declining to 9.84 per cent, while the industrial sector’s share increased to 38.34 per cent.

Credit, investment and fiscal position

Bank deposits continued to rise in October and November, with year-on-year growth reaching 10.8 per cent in November. Public-sector credit expanded rapidly to 23.24 per cent, reflecting increased government borrowing.

By contrast, private-sector credit growth remained subdued at 6.58 per cent, pointing to weak private investment amid uncertainty and tight financial conditions.

For FY2025-26, the revised revenue target was set at Tk 5.54 lakh crore. Revenue collection in December stood at Tk 36,191 crore, falling short of the revised monthly target by Tk 15,174 crore, although collections improved significantly compared with November and on a year-on-year basis.

The Revised Annual Development Programme was finalised at Tk 2.0 lakh crore, down from Tk 2.3 lakh crore in the original ADP, reflecting fiscal pressures and implementation challenges. Allocations rose in sectors with stronger execution capacity, including Environment, Forestry and Water Resources and Local Government and Rural Development, while major cuts were made to health, transport, education and energy.

Despite the reduced allocation, the number of approved projects increased, indicating a broader but more tightly funded development programme.

External sector resilience

The external sector showed signs of resilience during the first half of FY2025-26. Foreign exchange reserves strengthened, with gross reserves rising to $33.19 billion in December. Remittance inflows also grew strongly, reaching $3.22 billion, supported by regulatory incentives and a more market-aligned exchange-rate regime.

Export earnings stabilised at around $4.0 billion per month, with the RMG sector remaining the dominant contributor. Import payments remained volatile, while capital machinery imports stayed subdued, reflecting weak private investment sentiment.

The exchange rate remained broadly stable in December, with easing appreciation pressures in real effective exchange rate (REER) terms.

Outlook

While the 5 per cent growth projection for 2026 points to economic resilience, the GED cautioned that sustaining momentum will require faster reforms, stronger institutions and decisive policy action to rein in inflation, revive private investment and ensure inclusive growth as Bangladesh transitions beyond LDC status.

Source: UNB