Cotton conundrum Bangladesh's $5b import bill persists as domestic production stalls

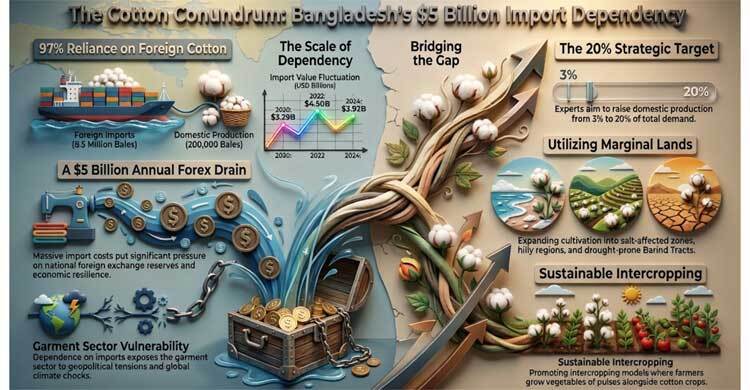

Bangladesh stands as a global paradox in the textile value chain: the world's second-largest exporter of ready-made garments yet reliant on imports for 97 per cent of its most critical raw material.

With annual cotton demand hovering around 8.5 million bales and domestic output barely scratching 2,00,000 bales, the nation's heavy dependence on foreign supply chains is raising urgent questions about economic resilience, foreign exchange pressure, and long-term industrial strategy.

Bangladesh has, on several occasions, overtaken China as the world's largest cotton importer. According to a 2025 report by the Bangladesh Agricultural Economics Institute, analysing National Board of Revenue data, the country spends between $4 billion and $5 billion annually on cotton imports.

The figures reveal a persistent and costly dependency. In 2020, Bangladesh imported 6.5 million bales at a cost of $3.29 billion. The following year, expenditure surged to $4.72 billion, before moderating to $4.50 billion in 2022 and $4.02 billion in 2023.

Most recently, in 2024, the country imported 8.3 million bales valued at $3.92 billion. These fluctuations reflect global market volatility, yet the underlying trend remains unchanged: domestic production meets only a fraction of industrial need.

Cotton is currently cultivated on approximately 50,000 hectares across 39 districts, primarily in char lands, hilly regions, and the drought-prone Barind Tract. Four adapted varieties are grown: char cotton for riverine islands, hill cotton for elevated terrain, upland cotton for the plains, and drought-tolerant strains for the Barind area.

Yet even with incremental expansion in cultivated area, output has plateaued between 2,00,000 and 2,20,000 bales annually.

At 182 kg per bale, this translates to roughly 40,000 tonnes, a mere fraction of the 1.5 million tonnes required by the country's 519 textile mills.

Industry observers point to several systemic constraints that have kept local production stagnant. Land scarcity presents a fundamental challenge, as intense competition for arable land from food crops makes it difficult for cotton to secure viable acreage. Research gaps also play a role, with critics arguing that the Cotton Development Board lacks effective, outcome-driven programmes to develop higher-yielding, climate-resilient varieties.

Policy and allocation shortfalls further compound the issue; despite annual budgetary allocations for seed distribution, farmer training, and ginning support, implementation has reportedly fallen short of targets. Finally, without competitive pricing or guaranteed offtake, many smallholders prefer more predictable crops such as rice, maize, or vegetables.

Established in 1972 and entrusted with cotton research in 1991, the Cotton Development Board carries the statutory responsibility for boosting domestic production, developing new varieties, and supporting farmers through technology transfer and market linkages.

To date, the board has released 24 high-yielding varieties, including the CB series (CB-12 through CB-18), CDB Cotton-19 to CDB Cotton-21, Pahari Cotton-3, and the hybrid CB Hybrid-1. It also promotes intercropping models, encouraging farmers to grow vegetables, pulses, and spices alongside cotton to maximise land productivity.

Rezaul Amin, Executive Director of the Cotton Development Board, acknowledged the challenges while outlining ongoing efforts. He stated that production is being increased through hardy, high-yielding varieties and climate-friendly technologies, with cultivation expanding into low-yielding lands such as the Barind Tract, salt-affected zones, pastures, agroforestry systems, and hilly areas.

He added that intercropping initiatives are gaining traction, offering supplementary income and improving soil health. However, he conceded that land scarcity imposes a hard ceiling on expansion.

Even with strong effort, achieving more than 10 to 15 per cent of national demand is not feasible under current realities, though the board's medium-term target is to reach 20 per cent. This ambition, he noted, requires coordinated policy support, sustained research investment, and deeper farmer engagement.

The $4 to $5 billion annual outflow for cotton imports represents a significant pressure on Bangladesh's foreign exchange reserves, particularly amid global currency volatility and rising freight costs.

Moreover, heavy reliance on imported cotton exposes the garment sector to supply chain disruptions, whether from geopolitical tensions, climate-related crop failures in source countries, or shifts in international trade policy.

Analysts warn that without a credible strategy to enhance domestic raw material security, Bangladesh's garment industry, which accounts for over 80 per cent of the country's export earnings, remains vulnerable to external shocks.

One Dhaka-based textile economist, who requested anonymity, observed that every dollar saved through import substitution is a dollar retained for infrastructure, skills development, or technology upgrading. Even a modest increase in local cotton production could yield meaningful foreign exchange savings and strengthen supply chain resilience.

For the 2025-26 fiscal year, the Cotton Development Board has set a cultivation target of 48,000 hectares, aiming to produce 252,000 bales. While this represents a marginal increase over previous years, it still accounts for less than 3 per cent of total demand. Experts suggest a multi-pronged approach could help narrow the gap.

Targeted research investment should prioritise drought-tolerant, short-duration, and pest-resistant varieties suited to Bangladesh's agro-ecological zones. Incentive structures, such as minimum support prices, crop insurance, and contract farming arrangements, could de-risk cotton cultivation for smallholders. Public-private collaboration might leverage textile mills' procurement power to create guaranteed offtake mechanisms for locally produced cotton.

Finally, sustainable intensification through agroecological practices could promote cotton in marginal lands while enhancing soil health and water efficiency.

Bangladesh's cotton story is one of missed opportunity and strategic urgency. While the nation has mastered garment assembly and export logistics, its inability to scale domestic raw material production leaves a critical vulnerability in an otherwise formidable industrial ecosystem.

With global cotton markets growing increasingly volatile and climate pressures mounting, the question is no longer whether Bangladesh can achieve self-sufficiency, as most experts agree that is unrealistic, but whether it can realistically raise domestic contribution to 10, 15, or 20 per cent of demand.

The answer will depend less on isolated interventions and more on a coherent, long-term national strategy that aligns agricultural policy, research investment, and industrial planning.

For a country whose economic aspirations are woven tightly into the fabric of global fashion, getting cotton right is not just an agricultural issue; it is a business imperative.